Published: March 25, 2026 | Format: Company Profile | Reading time: 9 minutes Category: Companies & Startups

Baidu and Tencent are two of the oldest names in Chinese tech. Both are betting heavily on AI. But their strategies could hardly be more different. Baidu is building vertically — from model to search to autonomous driving. Tencent is building horizontally — embedding AI into the world’s most-used messaging ecosystem. This article compares both approaches and asks: which one matters more for Europe?

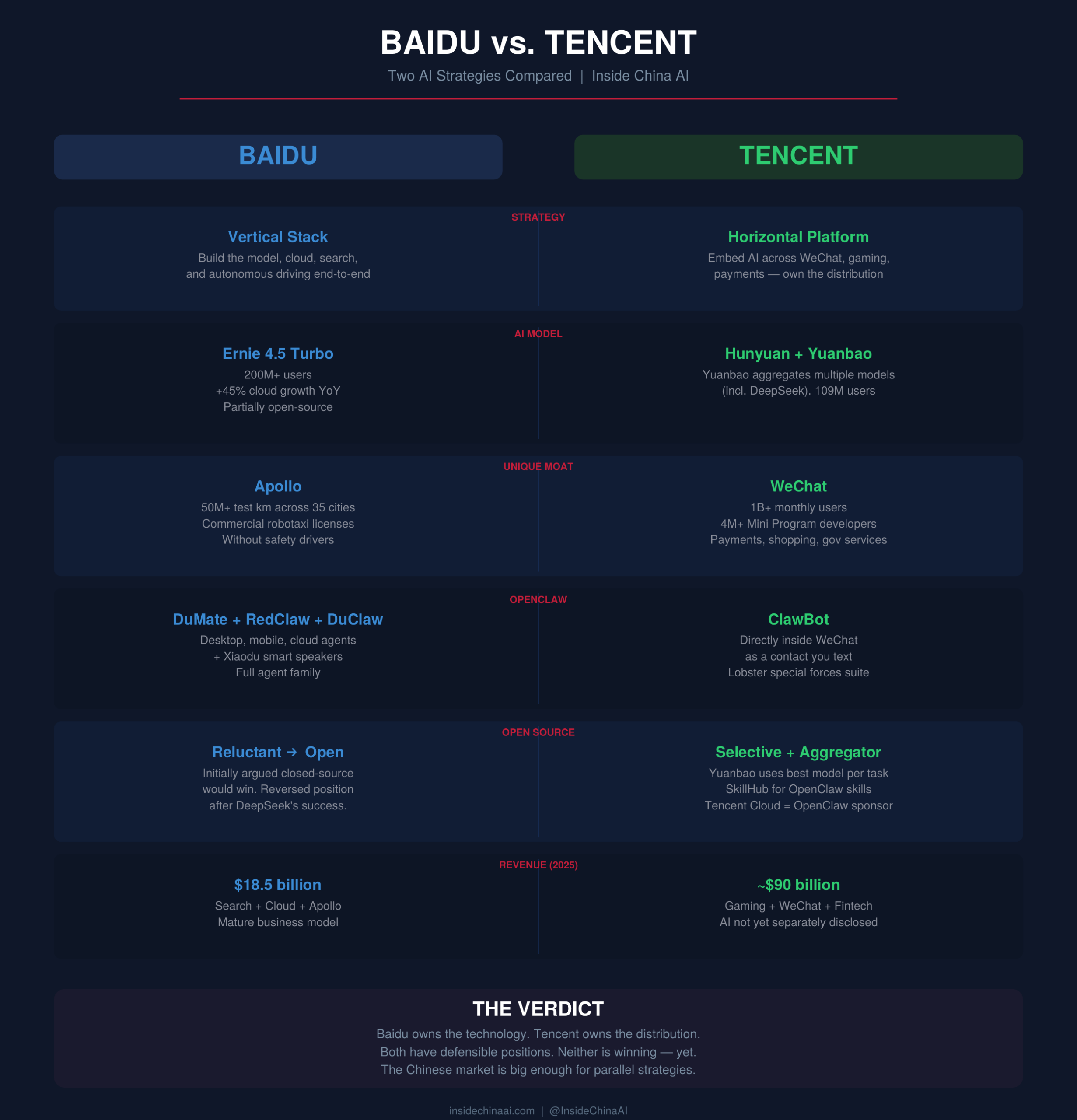

The Two Companies at a Glance

| Baidu | Tencent | |

|---|---|---|

| Headquarters | Beijing | Shenzhen |

| Founded | 2000 | 1998 |

| Core business | Search engine, cloud, autonomous driving | Messaging (WeChat), gaming, fintech |

| AI model | Ernie / Wenxin Yiyan (文心一言) | Hunyuan (混元) |

| Model name meaning | „Spirit of language, one word“ | „Primordial chaos“ (Daoist concept) |

| Users | 200M+ (Ernie Bot) | 1B+ (WeChat), millions (Yuanbao) |

| AI cloud growth | +45% YoY (Q1 2025) | Not separately disclosed |

| Open source stance | Initially closed → partially opened | Partially open + aggregator approach |

| Unique asset | Apollo autonomous driving | WeChat ecosystem (1B+ users) |

Baidu’s Strategy: The Vertical Stack

Baidu’s AI strategy is vertical integration. The company controls the entire stack: the model (Ernie), the cloud infrastructure (Baidu AI Cloud), the search engine (Baidu.com), and the autonomous driving platform (Apollo). Each layer feeds the others.

Ernie: The Model

Ernie Bot (文心一言) launched in March 2023 and was one of the first major Chinese LLMs. With over 200 million users, it remains one of the most widely used AI applications in China.

The latest release, Ernie 4.5 Turbo, focuses on enterprise needs: 40% faster inference than Ernie 4.0 at roughly half the per-token cost. This is a direct response to DeepSeek’s price disruption — Baidu can’t afford to be the expensive option when free alternatives exist.

Baidu’s open-source journey has been reluctant. CEO Robin Li argued publicly in early 2025 that closed-source models would dominate long-term. DeepSeek’s success forced a reversal. Baidu has since opened parts of its model family, though it remains less open than Alibaba’s Qwen or DeepSeek.

Apollo: The Autonomous Driving Bet

Baidu’s most distinctive asset is Apollo, its autonomous driving platform. With over 50 million test kilometers driven across 35 cities, Apollo is one of the world’s most advanced robotaxi programs. Baidu has secured commercial licenses to operate driverless vehicles in multiple Chinese cities — something even Waymo hasn’t fully achieved in the US.

Apollo matters for the AI strategy because it generates enormous amounts of real-world data that feeds back into Baidu’s model training. It’s also the strongest argument for Baidu’s relevance beyond language models: while chatbots commoditize, autonomous driving remains a frontier problem with high barriers to entry.

Search + AI Integration

Baidu’s original business — search — is being reinvented as an AI-first product. Ernie is increasingly the default interface for Baidu searches, providing synthesized answers rather than link lists. This mirrors Google’s approach with AI Overviews, but Baidu has moved faster because Chinese users adopted chatbot-style search more readily.

The integration creates a flywheel: search queries improve the model, the improved model drives more search usage, and both generate data that enhances the cloud AI services Baidu sells to enterprises.

The Vertical Logic

Baidu’s bet is that owning the full stack creates compounding advantages. Better search data → better models → better autonomous driving → more data → better cloud services. Each business strengthens the others.

The risk: this strategy requires excellence at every layer. If Ernie falls behind Qwen in model quality, or if Apollo loses ground to competitors like Pony.ai, the vertical stack becomes a chain that’s only as strong as its weakest link.

Tencent’s Strategy: The Horizontal Platform

Tencent’s approach is fundamentally different. Rather than building a vertical stack, Tencent is embedding AI horizontally across its existing ecosystem — the most extensive consumer platform in China.

Hunyuan: The Model (That You Might Not Use Directly)

Tencent’s Hunyuan model (混元) is technically capable, but it’s not designed to compete with Qwen or DeepSeek on benchmarks or downloads. Hunyuan’s purpose is to power Tencent’s products, not to win the open-source race.

The name itself — from Daoist philosophy, meaning the primordial undivided state before creation — suggests Tencent’s ambition: to be the foundational AI layer beneath everything, invisible but essential.

Yuanbao: The Aggregator

Tencent’s most interesting AI move isn’t its own model — it’s Yuanbao (元宝), an AI app that aggregates multiple models, including DeepSeek. Rather than insisting users adopt Hunyuan, Tencent built a platform where the best model for each task is selected automatically.

This is a typically Tencent approach: own the platform, not the technology. Just as WeChat became the platform for mobile payments without building a bank, Yuanbao positions Tencent as the AI gateway without requiring the best model.

The Lunar New Year campaign spent one billion yuan promoting Yuanbao with digital red envelopes — a direct echo of the 2014 WeChat Pay launch that disrupted mobile payments.

WeChat: The Distribution Advantage

Tencent’s real AI weapon is WeChat and its 1 billion+ monthly active users. The announcement that Hunyuan capabilities are now available within WeChat Mini Programs is potentially more significant than any benchmark result.

WeChat Mini Programs are app-like experiences that run within WeChat — over 4 million developers build on this platform. Giving every Mini Program developer access to LLM features means AI capabilities can reach hundreds of millions of users without anyone downloading a new app.

This is Tencent’s horizontal strategy in action: you don’t need to win the model race if you control the distribution.

Gaming + AI

Tencent is the world’s largest gaming company by revenue. AI integration in gaming — from NPC dialogue to procedural content generation to player behavior analysis — is a natural extension. While less visible than chatbots, gaming AI represents a significant revenue opportunity because gamers will pay for better experiences.

The Horizontal Logic

Tencent’s bet is that distribution beats technology. The best model in the world is worthless if nobody uses it. By embedding AI into WeChat, gaming, fintech, and entertainment, Tencent ensures massive adoption regardless of whether Hunyuan wins any benchmark.

The risk: this strategy depends on Tencent’s ecosystem maintaining its dominance. If a competitor disrupts WeChat (unlikely but not impossible), the distribution advantage evaporates. And if open-source models commoditize AI capabilities, Tencent’s aggregator approach might not generate enough value to justify the AI investment.

Head-to-Head Comparison

| Dimension | Baidu | Tencent |

|---|---|---|

| Model strategy | Build the best model | Build the best platform |

| Open source | Reluctant → partially open | Selective + aggregator |

| Distribution | Search (declining share) | WeChat (1B+ users) |

| Unique moat | Apollo (autonomous driving) | WeChat ecosystem |

| Revenue model | Cloud AI + advertising | Platform fees + gaming |

| Enterprise play | Strong (Baidu AI Cloud) | Growing (via Mini Programs) |

| International presence | Limited | Limited (except gaming) |

| Data advantage | Search + driving data | Social + payment + gaming data |

Who Is Winning?

It depends on how you define winning.

By model quality: Neither leads — both trail Alibaba’s Qwen and DeepSeek in open-source adoption and benchmark results. Baidu has a stronger standalone model; Tencent has a smarter distribution strategy.

By user reach: Tencent, decisively. WeChat’s 1 billion users dwarf Ernie Bot’s 200 million. But user reach doesn’t automatically translate into AI revenue.

By strategic positioning: Both have defensible positions. Baidu’s vertical stack (search + cloud + autonomous driving) is unique. Tencent’s horizontal platform (messaging + payments + gaming + AI) is unique. They aren’t really competing with each other — they’re competing with Alibaba and ByteDance for different parts of the value chain.

By revenue from AI: Too early to tell. Neither company has disclosed standalone AI revenue figures that would allow a fair comparison.

What This Means for Europe

Neither Baidu nor Tencent has significant direct European presence in AI — unlike Alibaba Cloud, which operates European data centers. But both matter for European observers:

Baidu matters for autonomous driving. Apollo is one of the world’s most advanced AD platforms. European automakers and mobility companies should understand where Baidu is and where it’s heading. If Apollo’s technology reaches European markets (directly or through licensing), it will reshape the competitive landscape.

Tencent matters for platform strategy. The WeChat Mini Program + AI integration model is a preview of how AI might be distributed at scale. European companies building AI features into their apps can learn from Tencent’s approach to platform-level AI embedding — even if the WeChat ecosystem itself is China-specific.

Both matter for understanding China’s AI ecosystem. DeepSeek and Alibaba get the headlines. But Baidu and Tencent, with their massive user bases and diversified businesses, are equally important players whose strategies shape the entire market’s direction.

The broader lesson: There is no single winning strategy in Chinese AI. Vertical integration (Baidu), horizontal platform (Tencent), ecosystem commerce (Alibaba), and pure research (DeepSeek) all coexist. This diversity is itself a strength of the Chinese AI ecosystem — and a contrast to the more concentrated Western market.

Sources: Baidu Q4 2025 earnings, Tencent Annual Report 2025, SCMP Tech, Reuters, Bloomberg, TechNode, company product announcements. Market share figures based on industry estimates.

No responses yet